Current Las Vegas Market Individual Charts

Current Las Vegas Market Report

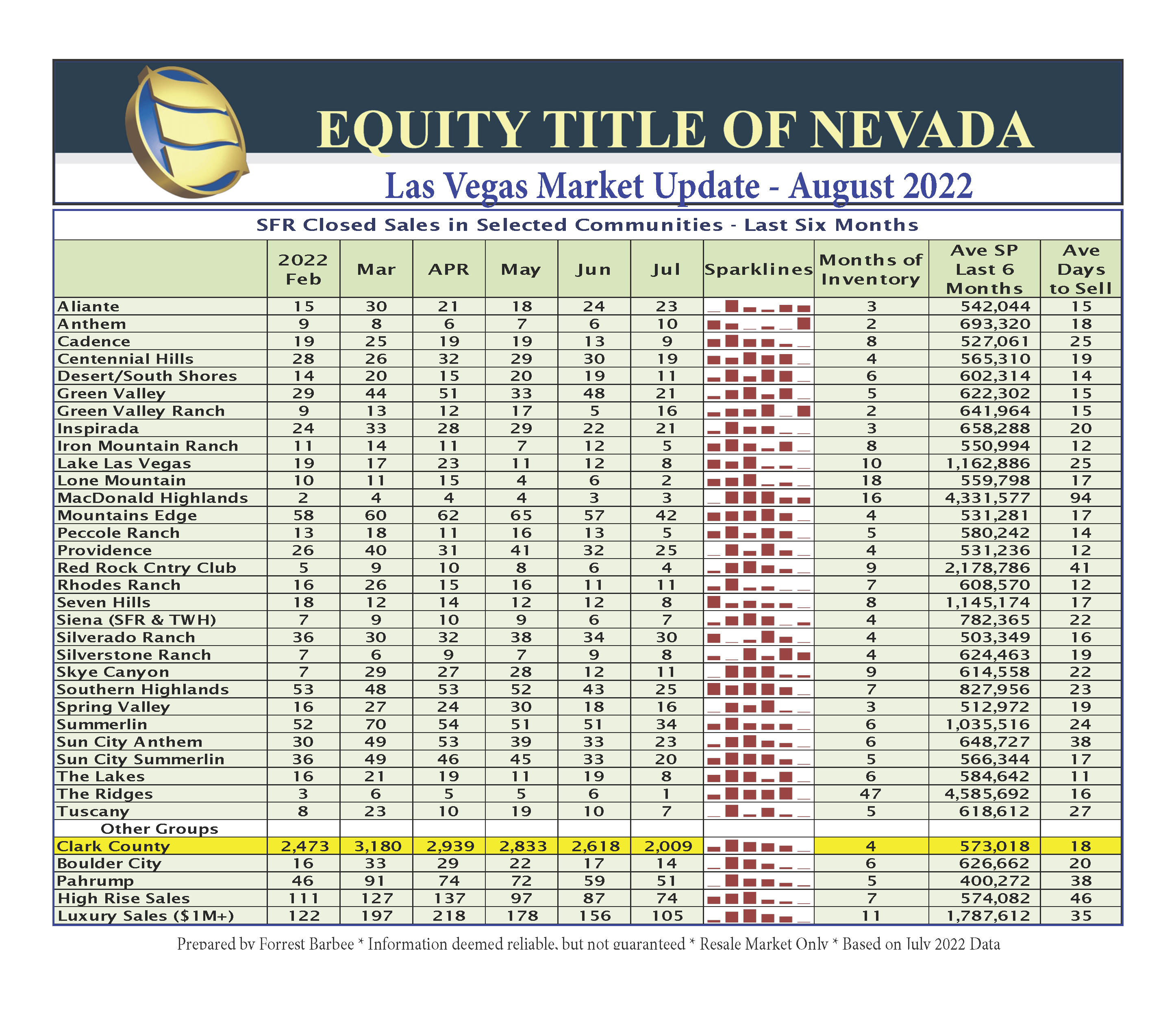

Market Overview

2022 closings are now 14.9% off the 2021 pace but is tracking closely to the 2019 market; closings at this pace could easily end up at 32,000 – 35,000 by the end of the year. Available SFR inventory improved from 6362 units to 7895 units while listings taken in July were approximately 380 less than in June. The SFR market sits at 3.9 months of available inventory even as the condo and townhome segment rose to 2.9 months of inventory. The average days on market inched up to 18 days. This metric should be rising but so many “older” listings are constantly being relisted to create the impression that the listing is new by reflecting fewer days on the market.

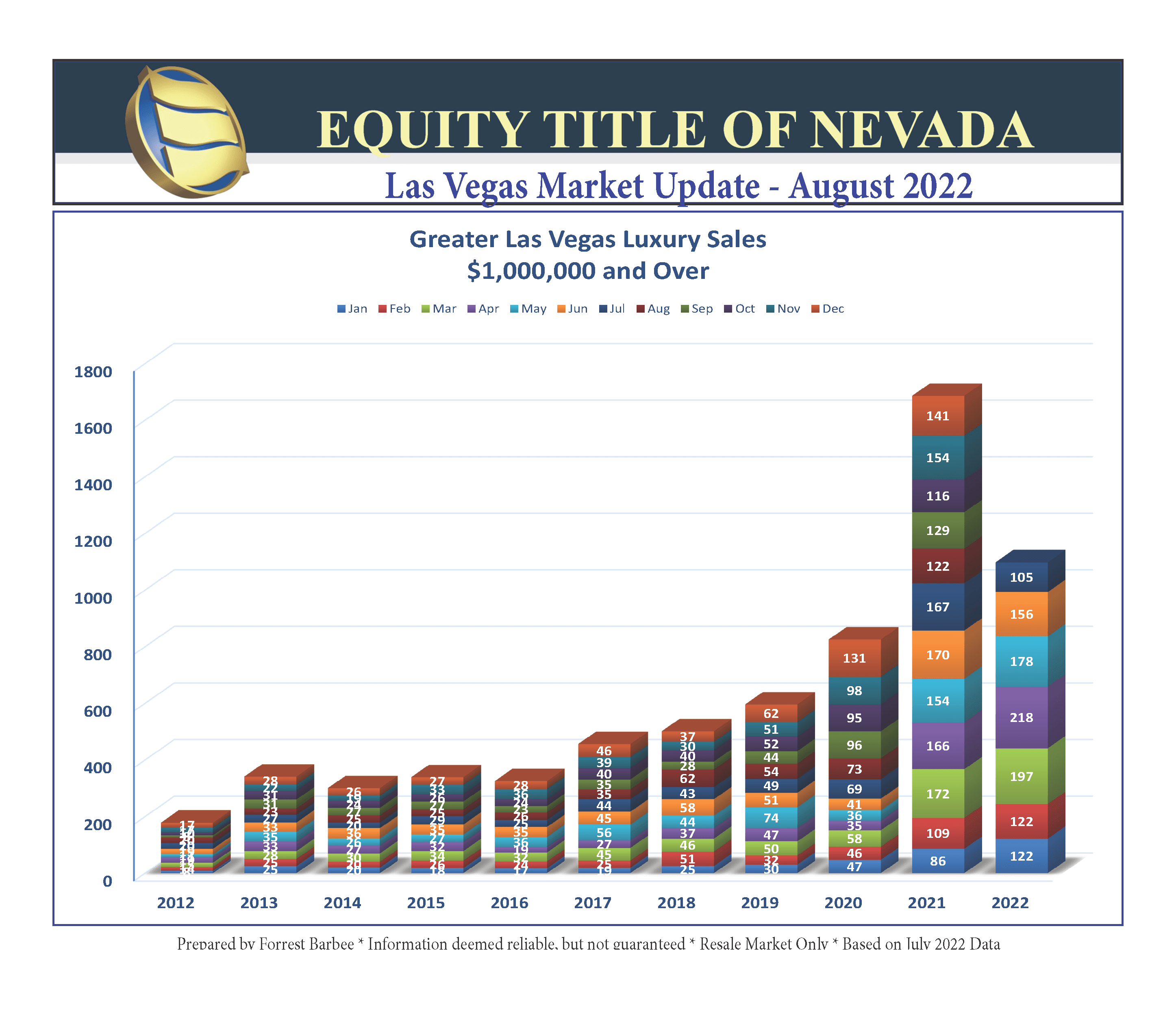

The median sales price of SFR closings dropped to $465,000 from $480,000 while the SFR average closed sales price fell from $593,941 from $544,598 for a one-month decrease of 8.3%. The very high end of the luxury market had slightly fewer closings that last month, but overall closings above $700,000 remain reasonably strong. Clearly, more closings are occurring at lower price points. One caution – this does not mean that market prices are falling! Buyers who need financing may – of necessity – be looking for their next home at a price point lower than they would have been searching for only six months ago. They will still be paying market value, but at a lower price point.

Market Prices

The real estate market is rapidly returning to normal conditions where both buyers and sellers have a more equal ability to negotiate that dream home. The Las Vegas market rose to nearly four months of SFR inventory which is in the zone where the market is considered balanced. Generally, neither party has inherently more ability to negotiate than the other when there is 3 to 6 months of inventory. The first casualty in a balanced market is the ability of sellers to compel buyers to pay over and above market prices and/or appraised values. This does not lower market values, but merely returns more closings to existing market/appraised values.

Clearly a balanced market is most welcome as it will slow down the double digit rise in market values and squeeze out the overpricing. Listing agents may need to get a grip of the shift and hone their sales and negotiating skills while adapting to these changes. However, that’s the macro-view of the market. The chart below shows that various communities around the valley are each responding to the market changes in their own way – with a dramatic range in months of inventory. Some communities have two months of inventory while others range up to 18 months of inventory. Thus, a buyer’s or seller’s ability to negotiate will be – to some extent – tied to these numbers as they reflect each community’s supply and demand position. Seller’s whose circumstance are such that they cannot wait 8, 10 or even 16 months to sell may need to consider lowering their asking prices if their motivation to sell is more urgent! This is an event that could result in lower market values in some communities.

It’s time for all of us to adopt a change in mindset that reflects the current market and economic conditions in the specific market areas we work. Temper news and media reports on the market with that in mind. Then pass accurate market conditions on to your clients and prospects! This market is replete with opportunity

Property Management Permit Pre-Licensing Class

24 Hour Online Format

Online Continuing Education Class – Broker Management