NVAR President for 2015!

NVAR President for 2015!

Congratulations to Kevin Sigstad on being installed Friday evening in Reno as our incoming NVAR President for 2015. Kevin will have a full plate and several balls to juggle as we brace ourselves for the upcoming Legislative Session beginning in February. Rest assured – some form of Service Tax will be back on the table. Moreover, this session will just as challenging as ever – despite the change in both the Assembly and the Senate. Therefore, please pay your PSF dues when paying your annual Board dues. Then consider increasing your PSF donations to Major Donor levels. This is the only way we defeat issues such as the MRP proposal in North Las Vegas or Question 3 during this last election.

The Current Las Vegas Market

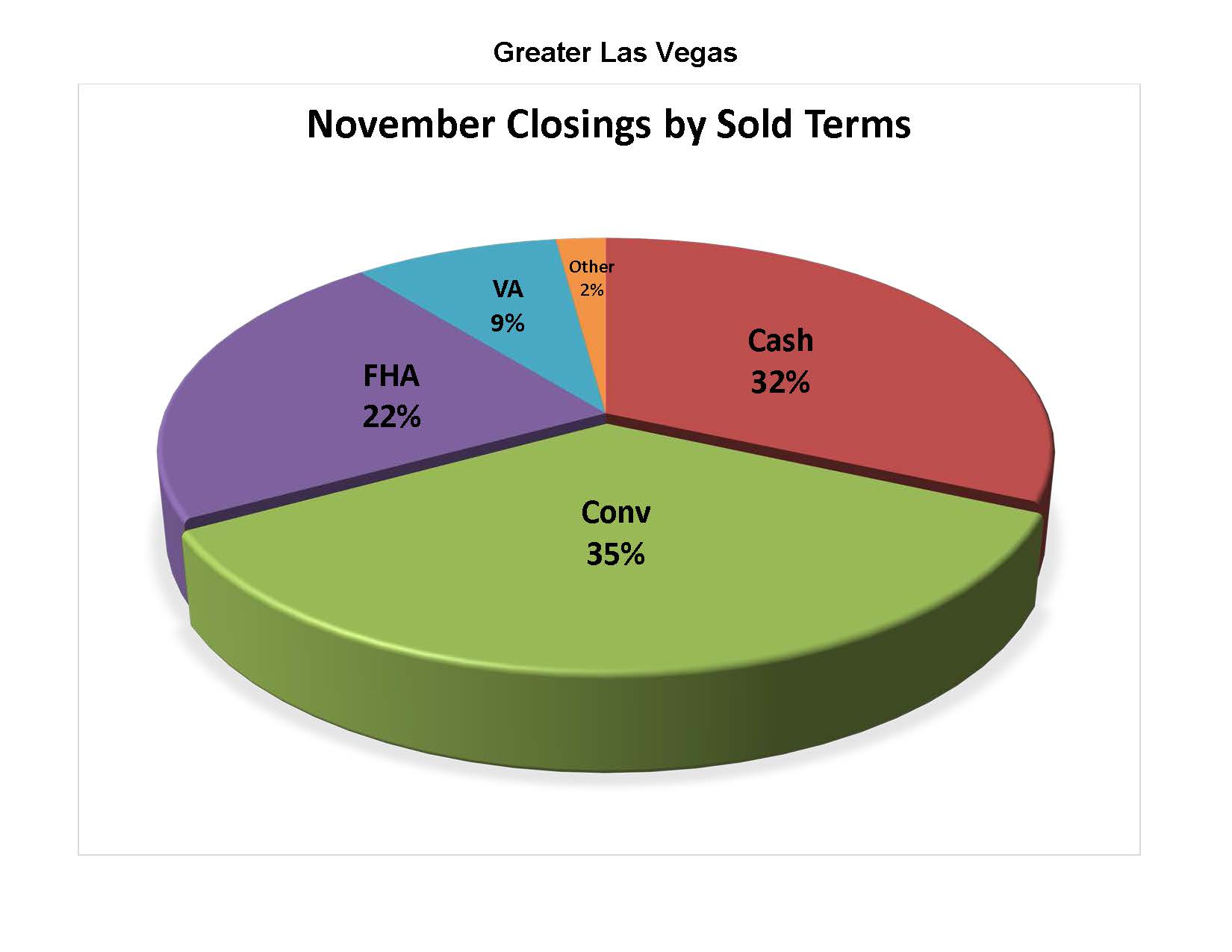

Closed sales for Year-To-Date 2014 remain 11.5% behind last year as we enter into November. The median sales price of an SFR improved to $202,000, while the average price settled in at $243,449. The Greater Las Vegas market now has a 4.1 month supply of Single Family Residences and a 5 month supply of Condos and Town-homes. 2014 continues to look remarkably like 2003. However, the most noteworthy change this month is the six percent swing away from cash closings in favor of conventional loan closings.

Admittedly, some of this change is a result of cash sales drying up to some extent, especially as investors have become more cautious in Las Vegas while researching alternative markets in Georgia, Texas, Oklahoma, and Iowa, and others. However, much of the market share improvement involving all forms of financing – including conventional financing – are the result of Las Vegas having made the transition to a non-distressed market with better underlying economic metrics.

Closed units remain down and there is nothing to suggest that this trend will turnaround any time soon. Yet, please keep in mind that we are closing more units in the $250K – $1M price points in 2014 compared to either 2012 or 2013. Commercial and property management activity have both increased in visibility as well. So there is every reason to believe that Sales Executives will do better in 2015, but it will require some business planning changes that embrace the market changes.

Click Here to Download the Current Las Vegas Market Update

Click Here for Additional Las Vegas Market Update Charts

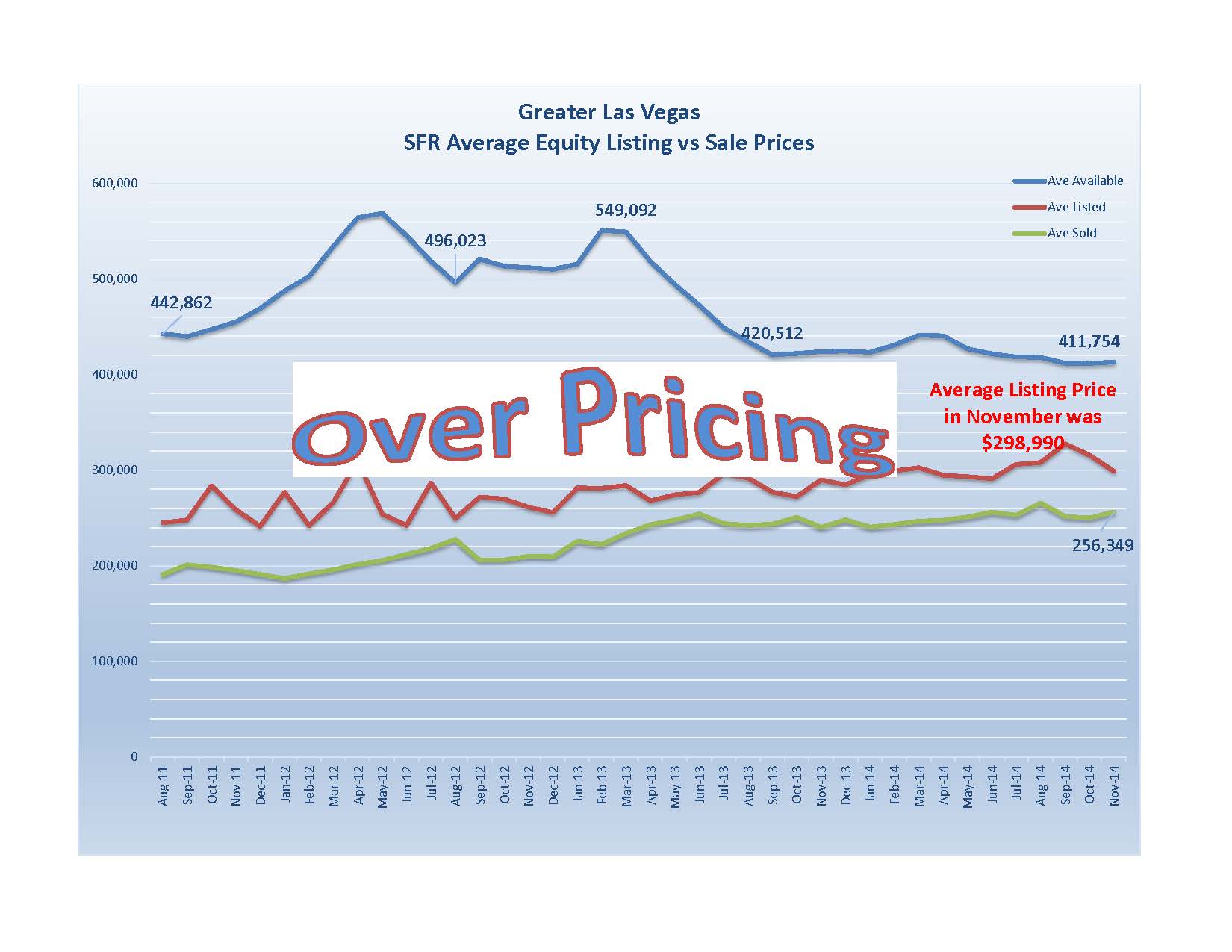

As always “all real estate is local”! Very local when evaluating Greater Las Vegas market pricing. Avoid over pricing your next listing! But now for some good news on that subject!

The red line indicates the average listing price of an SFR with Equity each month, while the blue line depicts the current average listing price of an SFR with Equity. November generally enjoy many closings with significantly fewer Days On Market than October. Buy why? For the past several months we have seen listing agents take listings priced closer to the market. In turn, the newer – better priced listings – are selling while the older, over priced inventory continues to stagnate. Still, the blue line clearly shows that we have a great deal of older, over priced listings that either need price reductions or need to come off the market.

Why is over pricing such a concern? Actually we have the same forces surrounding over pricing that swirled around us in 2003-2006. Thus the forces for creating another housing market bubble are truly in play. So what’s different and why do we not see a bubble forming? The market ten years ago had few if any checks balances to prevent the bubble. Fortunately, the current market experiences much more conservative and regulated appraisals. Secondly, mortgage underwriting remains tighter with more conservative requirements and the additional QM rules. So despite how challenging the appraisals and loan underwriting can be – we should be thankful they are there to prevent the next bubble. Working through an over pricing bubble is easier than paying the price for another housing market bubble.